How Are Those Tariffs Going?

The Inevitability of US Surrender Talks

As China has remained resolute, President Trump is already rolling back his rhetoric and is looking for a way out from the policy hole that he himself created. Once a bully understands that his threats are not working, and that his opponent has the upper hand and is resolute, he will climb down. Another embarrassing failure early in the Trump administration. Below I lay out the reality that the US, and US corporations, are facing if the tariff war is not quickly resolved.

It has now become obvious that the US administration wanted to create a cordon sanitaire around China to stall China’s onward economic development; using threats of crippling tariffs to bully other nations into cutting off China. The problem with this approach is that it is about two decades too late, as China is now the largest trading partner for Asia, Australia, Eastern Europe, the Middle East, Africa, and South America. China is also the dominant supplier of many, many critical inputs to other nation’s industrial processes, including those of the US. The Chinese Party-state has responded by making sure that everyone understands that it will take actions against nations that give in to the US bullying.

The view that the US can bring back the manufacturing industry that its oligarchs have spent many decades destroying and offshoring is delusional, as S. L. Kanthan notes for these ten reasons:

Wall Street and US corporate elites will not invest in manufacturing.

The US lacks skilled manufacturing workers.

Young Americans have no desire to work in factories.

Environmental laws are too strict.

The costs of labour and doing business are too high.

The US does not have good infrastructure, such as railways, seaports or even electricity.

The rules of the game could change quickly, for example if the Democrats win the mid-terms. Here, the sheer volatility of Trump himself does not help. Companies cannot make long term investments in such an environment.

Bullying will not work when the US is not ideal for manufacturing, if it was it would already be flourishing.

China, and Asia, have mastered the manufacturing supply chain.

You cannot reverse 45 years of de-industrialization.

To get to the position that it is currently in, it has taken China 45 years of highly competent and comprehensive economic and societal planning in an environment that was highly supportive due to the US opening up free trade for China, and the Western oligarch happiness to move their manufacturing to China. As T.P. Huang notes, China is now in its third phase of industrial development.

1980 - 2005

Provision of an endless supply of cheap labour for Western corporations to use as a base of cheap manufacturing, while China gained knowhow through Foreign Direct Investment and technology sharing. Much of Western thinking is still stuck in this period.

2005 - 2020

China becomes so good at manufacturing that Western corporations end up using China for all manufacturing, hollowing themselves out. In this period the vast amount of the profits still went to the Western corporations who controlled the brands, the IP and the supply chain - as with Apple. This is the period when Sean Starrs questioned whether China could ever overcome US power given that its more advanced manufacturing exports were still under the control of Western foreign enterprises. This also included the period of Trump’s first term.

2020 to Now

China has resoundingly answered Starrs. As T.P. Huang correctly stated, China had to move into a position:

where it controls the design, the technology and the supply chain so that Western companies cannot just get up and move that to another country. China had to be less reliant on foreigners and more on itself. It cannot rise to a great power and still [be] reliant [upon] foreign countries not turning hostile.

And that is exactly what it started to do. The pre-eminent example is that of the electric vehicle and battery industry where it is the Chinese owned companies that are now dominating - such as BYD, Geely, Chery, SAIC, Xpeng, Xiaomi, Huawei and CATL. Both Xiaomi and Huawei have much larger industrial and technological footprints, of which their EV successes are just a part. The same can be said for the whole “green” industrial sector. Also, in areas such as drones (DJI) and humanoid robotics, and China is rapidly catching up in chip manufacturing.

T. P. Huang

Operating in the global centre for manufacturing, which encompasses all parts of the manufacturing supply chain, Chinese companies have an unassailable advantage in the speed of new product design and introduction; as seen in the EV industry. Within the massive industrial clusters, such as that centred around Shenzen, companies can work very directly with all parts of the supply chain. Something that is simply not available to corporations not located in such clusters. Because of this:

Product iteration time for a company in Shenzhen or Hangzhou is so fast. They have full access to ppl that design boards, understands mfg process, can buy all the ICs/parts & that do multi-modal small models. There is no language or timezone barrier. How to compete w/ this? For example, if you are in North America, how do you source the right battery for your electronic device? When the any supply chain and manufacturing know how exist in 1 area, you have to go there to work efficiently. As we head to a time when toys, appliances, consumer goods and machineries all become increasingly more electronic and smart, China has a distinct advantage in produce iteration. That’s what we have seen in EV industry, where China has clearly taken a multi-year lead. You can see that also in the exports. When China Inc starts to design the best product, then it also captures the entire value chain. Products will get cheaper globally, but Western designers will increasingly loose [sic] out.

China is rapidly moving up the value chain, with more labour intensive and less value-added work being off-shored to other parts of Asia; such as Vietnam. This produces a virtuous circle where such offshoring drives the economic development and rising living standards of Asia, which in turn drives Asian demand for Chinese products and Chinese investments. China is bringing both economic development and rising living standards to Asia and the rest of the non-Western world as it drives demand for commodity imports, exports its less value-added manufacturing, and provides products at cheaper prices to the world. This process is rapidly displacing Western corporations and Western influence. The recent Canton Fair showed the strength of China, as corporations from around the world flocked there to see the latest Chinese offerings.

The “dominate the supply chain while making everything in China/Asia and capturing most of the profits through colossal markups” strategy of so many Western corporations, including the sellers of luxury goods, now has a Chinese dagger pointed directly at its heart. As Chinese brands establish a stronger and stronger presence across the globe those incredibly fat profit margins will shrivel, and with them the earnings and price earnings multiples of Western share prices. We already see this in the automobile industry (excluding the Tesla bubble) and it will become apparent across one product sector after another. A reality which the YouTube channel “Inside China Business” has repeatedly pointed out. It is these profits that maintain the de-industrialized US.

As Warwick Powell details, we could also see a significant disintermediation of US retail platforms such as Walmart, Amazon, Target, Best Buy, and Foot Locker to bypass the usual 100% physical retailer markups and steep online seller markups and fees. By cutting these out, foreign manufacturers (especially the Chinese ones that provide about 60% of goods on Amazon and in Walmart) can maintain profitability while keeping prices relatively close to the pre-tariff level. The pressure will be immense to dis-intermediate the supply chain between manufacturers and the end customers. Platforms such as AliExpress, Temu, Shein, Alibaba and even TikTok shop could come out as big winners from this trend, with customers learning to accept slightly slower delivery times in exchange for a much lower price. US retailing provides 10% of the jobs in the US. As Powell puts it:

Before Trump’s tariffs, American OEMs and brands were perfectly content to outsource everything from design-for-manufacturing to tooling, to final assembly, to China. The strategic and value trade-off was clear: “Let Chinese firms do the hard, low-margin work, and we’ll capture brand value, IP rents, and global consumer markets.” This worked for decades, until it didn’t.

Trump’s first wave of tariffs in 2018-19 disrupted this set of quiet interdependent relationships. Chinese manufacturers were forced into the spotlight. They started to advertise their capabilities to the world. The ‘hidden secret’ of Chinese OEM capability was no longer a secret. Many began to pivot into direct-to-consumer brands, especially on Amazon and now TikTok …

Trump 1.0 and now Trump 2.0 is ushering in an era of supply chain disruption, but not in the way that was anticipated when policy-makers in Washington began talking about ‘bringing back manufacturing’. Manufacturing won’t be coming back to the United States any time soon in any great quantity. But the supply chain disintermediation sparked by the introduction of tariffs will now affect both the upstream sources of American economic value (namely in design, brand ownership and IP rents) and the downstream systems of retailing.

The US tariff and export-control bullying comes at just the time when China is making itself independent of the West, and the nations of the rest of the world outside the West increasingly have another alternative to the West. One that does not interfere in their internal affairs and tends to bring development, upgraded infrastructure, cheaper products, and even financing without the usual IMF/World Bank “structural adjustment” conditions. Making matters worse for the US is the combination of gross incompetence and overweening arrogance of a US administration that has picked a tariff fight with the whole world.

A number of foreign trade delegations have already expressed their frustrations that the US administration cannot tell them what it wants, while it also overreaches for significant interference in the internal functioning of other nations; such as questioning Value Added Taxes, food regulations, and nation’s own relationship with China. At the same time China has shocked the assumptions of the US administration by directly retaliating with 125% tariffs on imports from the US, and with a refusal to negotiate until the US shows some basic level of respect and diplomatic competence. At the same time, it is offering free trade to other nations and has even excluded components produced in Taiwan from the tariffs on US imports as that nation is deemed to be part of China; greatly complicating the US attempts to move chip production from Taiwan to the US. In addition, the recent success of Huawei with AI chip sets, together with further US restrictions on chip exports to China, has already driven the founder of Nvidia to visit China and talk about the wonderful relationship that he wants to continue with the country.

As China stands firm, and other nations also do not bend to the US bullying, the effects of the tariffs will work their way through the US economy. First with the Western US sea ports, then through the transport infrastructure of trucks and railways, and then onto the shelves and production lines of US companies. As shortages ripple through the US economy, inflation will spike while production falls. More and more US companies will be warning of supply chain issues, while the US agri-business sector collapses as its biggest export market has disappeared. Just as all this is happening, the Trump administration has exacerbated the economic fallout through its xenophobic and arrogant attitudes toward immigrants, visiting business people and academics, and even vacationers. The US foreign tourist and educational industries will take a severe hit from the masses that stay away due to not wanting to deal with the empowered ICE (Immigration & Customs Enforcement) bigotry and arrogance, and not wanting to reward the Trump administration’s insults, threats and bullying. There will also be long-term damage to US research and innovation, as foreign researchers and skilled workers increasingly see the nation much less as a “promised land” and more as a xenophobic and racist one that is better steered clear of.

The US financial markets had started trading more like those of an emerging economy, as the dollar and the stock market fell while interest rates rose. Trump then started to publicly bad mouth the Fed governor who sees the need to hold interest rates steady with the tariff-induced incoming inflation, raising the possibility of 1970s style stagflation. At risk is emerging-markets style capital flight that would produce a rapid financial crisis within the US. As Pepe Escobar notes below, the Chinese leadership and population are defiant and will not yield as the effect of the tariffs work their way through the US economy. This will continuously increase the pressure upon the Trump administration to find a way to quietly surrender. The utter idiocy and arrogance of Trump in his statements about China, and even a Vice President that described the Chinese as “peasants”, has not helped the US cause

It has now come out that the Treasury Secretary Bessent is utterly blinded by an ideologically-driven anti-China bias, even to the point of rejecting any articles that were positive about China at the think tank that he previously headed. At the Institute of International Finance Bessent stated the following:

China can start by moving its economy away from export overcapacity, and toward supporting its own consumers and domestic demand. Such a shift would help with the global rebalancing that the world desperately needs.

Of course, trade is not the only factor in broader global economic imbalances. The persistent over-reliance on the United States for demand is resulting in an evermore unbalanced global economy.

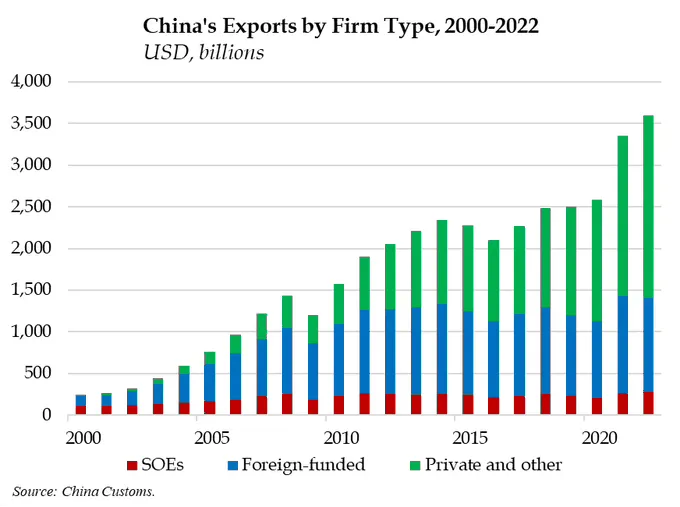

The US share of China’s total exports fell from 18% in 2017 to only 14.7% in 2024 (2.33% of Chinese GDP), while the Chinese share of total US imports fell from 21% to 13% during the same period. China has been reducing its dependence on the US for demand, with only 2.33% of GDP now directly dependent upon such US demand. During the same period, China has greatly expanded its exports to the global south at the cost of Western exporters. In 2017, Chinese imports from the US were worth US$130.4 billion, and in 2024 US$143.5 billion. A reduction as a share of Chinese GDP, and predominantly easily replaceable agricultural products, fossil fuels, chemical products and metals. In 2023 Chinese retail sales increased by 7.2%, in 2024 by 3.5%, and at a 4.6% annualized rate in Q1 2025; hardly showing a country with a domestic demand issue.

The statements of the Treasury Secretary are utterly disconnected from reality, placing him in the same camp as the President, the VP, and the anti-China lunatic Commerce Secretary. None of them have ever been involved in manufacturing, nor worked on an industrial development plan. They have now entered a period of a very severe and painful “learning experience”, which may unfortunately produce very negative consequences across the United States.

Let’s remember that China already enjoys free trade with the ASEAN nations of Brunei, Cambodia, Indonesia, Laos, Malaysia, Myanmar, Philippines, Singapore, Thailand and Vietnam. In early July this year, the BRICS countries of Brazil, Russia, India, China, South Africa, Egypt, Ethiopia, Indonesia, Iran and the United Arab Emirates will meet in Brazil. The BRICS partner countries of Belarus, Bolivia, Kazakhstan, Cuba, Malaysia, Thailand, Uganda, Uzbekistan and Nigeria will also be in attendance. This will be an excellent opportunity for the non-Western nations to coordinate their response to the US aggression.

Trump has now walked back his threats to fire the Fed Governor, and is now softening his rhetoric toward China as he looks for a way out from his self-created problem.

I would not be surprised if the Chinese drag this process out, as Trump is hoist on his own petard as the negative effects work their way through the US economy. On a strategic level though, China wants to manage the relative decline of the US at a controlled pace that will not trigger global economic fallout or outright conflict. There will be some resolution, but the relationship between China and the US has been forever damaged while China has gained geopolitical capital by resolutely standing up to the Trump administration. The controls on the export of Chinese strategic minerals may also be kept in place, as a way of limiting any US military build up and slowing US high technology developments.

With the probable failure of the Ukraine War negotiations, the tariff climb down with respect to Mexico and Canada, the tariff retreat with respect to electronic imports from China, and now Trump setting the stage for a more general tariff retreat with respect to China, the Trump administration has been significantly weakened within its first few months. Not helped by the actions of DOGE (Department of Government Efficiency) and ICE (Immigrations and Customs Enforcement) that have negatively affected members of the MAGA (Make America Great Again) core constituency. A recent CNBC poll found that Trump had a negative approval rating with respect to his handling of the economy, a first for both his first and second terms in office; after only three months of his second term.